The Fed has different priorities than the ECB, the Bank of Japan, the Swiss National Bank, et al.

During the press conference today following the FOMC meeting, Fed chair Jerome Powell was asked if and when the Fed would push its policy interest rate into the negative. Powell did not respond with his usual, “we will act as appropriate.” He had a real answer.

For months, there has been clamoring from Wall Street and speculators, and from the White House, that the Fed should or would cut its policy rates into the negative. Peak of the negative-interest-rate momentum was likely in late August or early September.

Since then, longer term yields have risen across the board, and a substantial part of the $17 trillion in negative yielding debt has turned into slightly positive-yielding debt. So maybe folks are worried that the negative interest rate era is coming to an untimely end, and they want the Fed to step in and save the day.

At the post-FOMC meeting press conference, negative interest rate policy (NIRP) came up in the context of the Fed’s blowing its firepower with these rate cuts before there is even a recession; and then not having much firepower left when that recession arrives. Powell was asked directly about it: Is there “any scenario in which you would envision rates drifting lower into negative territory, and are there any other tools that you could use before having to go there?”

And Powell replied:

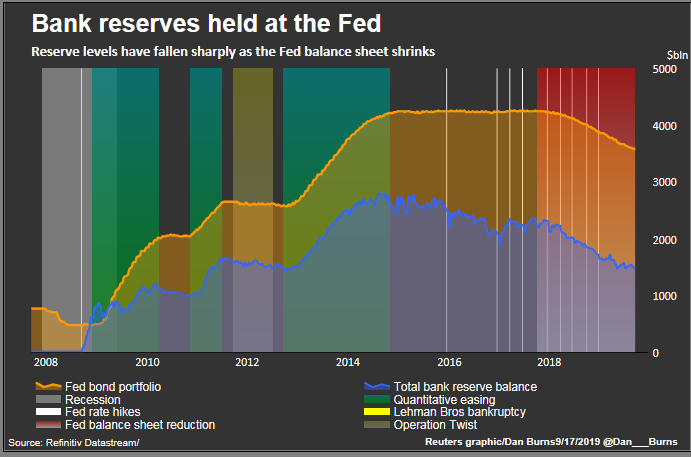

“Negative interest rates is something that we looked at during the financial crisis and chose not to do. After we got to the effective lower bound [near-zero effective federal funds rate], we chose to do a lot of aggressive forward guidance and also large-scale asset purchases.

“Those were the two unconventional monetary policy tools that we used extensively. We feel that they worked fairly well.

“We did not use negative rates. And if we were to find ourselves at some future date again at the effective lower bound – not something we are expecting – then I think we would look at using large-scale asset purchases and forward guidance.

“I do not think we’d be looking at using negative rates.”

So negative interest rates are not happening. Over the years, other Fed officials have expressed their unwillingness to deploy negative interest rates as well – and for good reason.

Negative interest rates are even worse than near-zero interest rates. They have not proven to be beneficial for the economy anywhere where they’re currently in operation, and they entail seriously destructive side effects for the people and the banking system in the country.

However, negative interest rates as follow-up and addition to massive QE were effective in keeping the Eurozone glued together because they allowed countries to stay afloat that cannot, but would need to, print their own money to stay afloat. They did so by making funding plentiful and nearly free, or free, or more than free.

This includes Italian government debt, which has a negative yield through three-year maturities. The Italian 10-year yield is only 0.9%, rather than 7% or 8%, as it was during the Debt Crisis, when Italy was approaching a default, like Greece had already done. The ECB’s latest rate cut, minuscule and controversial as it was, was designed to help out Italy further so it wouldn’t have to abandon the euro and break out of the Eurozone.

The US doesn’t need negative interest rates to stay glued together. It can print its own money.

In Switzerland, Denmark, and some other countries, negative yields are used as blatant currency manipulation, to push down their currencies. That would be tempting for the US as well, but then there is a price to pay – as we can see from the economic doldrums and the banking fiasco in Europe and Japan.

Negative yields have been another blow for the European and Japanese banks hobbling from crisis to crisis, their shares wobbling along multi-decade lows. Negative yields are the final blow for pension and retirement systems. Negative yields distort the pricing of risk, and therefore distort the cost of capital and lead to business decisions that would otherwise be idiotic waste and malinvestment. This is an issue that is already playing out with low interest rates – such as share buybacks funded with borrowed money – and it gets a lot worse with negative interest rates.

The Fed is the guardian of the banks and has been created for the banks. The 12 regional Federal Reserve Banks are owned by the financial institutions in their respective districts. And a monetary policy that is damaging to the banks, undermines the banking system, and puts bank shareholders at risk of massive losses is just basic anathema to the Fed. Powell wasn’t the first one to just say no to NIPP, but he said clearly.

The 10-year Treasury yield rips. Unstoppable negative yields become stoppable. Read… THE WOLF STREET REPORT: Snapback Bloodletting in the Overripe Bond Market

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate “beer money.” I appreciate it immensely. Click on the beer mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

https://wolfstreet.com/2019/09/18/feds-powell-says-no-to-negative-interest-rates-at-next-recession/

2019-09-19 04:32:20Z

52780383489542

{kind=link}

{kind=link}