Federal Reserve chairman Jerome Powell has spent a year messaging confidence to investors in the heavily coded language of central bankers, and last month finally gave President Donald Trump the rate cut he'd been demanding for months.

Now Powell has a much tougher audience: American shoppers.

The thing keeping the US economy afloat despite Trump's ongoing trade wars and contractions overseas is consumer spending, which has stayed strong despite a slew of negative headlines -- a federal budget deficit topping $1 trillion, bond markets sending signals of a looming recession and now an oil shock in Saudi Arabia.

But any slip, especially heading into the holiday season, could mean the difference between a gentle slowdown and a full-blown recession.

"The one aspect of the US economy that's really holding up well is the consumer, and if the consumer gets freaked out and clutches the pocketbook tighter then a downturn becomes a self-fulfilling prophecy," Greg McBride, chief financial analyst for Bankrate.com told CNN.

In an internal webcast hours after the shared-workspace provider delayed its stock-market listing, Neumann said he had lessons to learn about running a public company, according to the Financial Times. He also voiced regret over how the listing process was handled, the newspaper said, citing people who saw the presentation.

Neumann's larger-than-life personality played a "huge role" in the listing's failure, the Financial Times reported, citing someone who worked closely with him. Fears of emulating the disappointing public debuts of Uber, Lyft, and other disruptive businesses this year factored into Neumann's decision to postpone WeWork's IPO, people close to the cofounder told the newspaper.

Neumann and two other WeWork executives vowed to employees the IPO would go through later this year, but the company could be forced to delay its public debut until next year, people briefed on the matter told the Financial Times. WeWork was expected to drum up interest in its shares during an investor roadshow this week, before listing them on the Nasdaq index next week.

Investors grew disillusioned with WeWork's unclear path to profitability, business model, complex structure, hefty valuation, and controversial governance. The group slashed its targeted public valuation to below $20 billion — less than half the $47 billion private valuation it secured in January — and introduced new limits on Neumann's control of the company, stock sales, real-estate deals, and succession plans, but failed to win enough support.

WeWork hopes a fresh set of quarterly financials for the three months to September will help it to revive its IPO next month, according to Reuters, citing people familiar with the company's thinking. However, investor demand could prove lackluster as fund managers become more conservative and look to protect their gains in the fourth quarter, Reuters said.

WeWork must raise at least $3 billion through an IPO this year, or it will lose out on a $6 billion credit line tied to that milestone, forcing it to seek alternative financing.

President Donald Trump has called Federal Reserve Chairman Jerome Powell 'clueless.' | Drew Angerer/Getty Images

President Donald Trump has taken over Jerome Powell’s life.

The Federal Reserve’s expected decision on Wednesday to cut interest rates again will spark new questions about whether Powell, its chairman, is caving to intense public pressure by Trump. While Powell strongly rejects that notion, the president’s policies have clearly forced the central bank’s hand.

Story Continued Below

The Fed, which last December was considering hiking interest rates at least twice this year, has done a head-spinning turn since then in response to weakening business investment, a contraction in manufacturing and a global slowdown — all fueled by Trump’s trade wars.

And the president’s abrupt decision last year to pull out of the Iran nuclear accord arguably set off a steady deterioration in relations that today has made Middle East tensions another threat to economic growth that the Fed must take into account.

Trump is forcing still more dramatic policy options into the limelight — including his latest call on the Fed to cut rates below zero, an idea that the central bank has long resisted as an avenue for fighting recessions.

“I’ve always thought the Fed has been a little bit slow to control the narrative about monetary policy,” said Seth Carpenter, chief U.S. economist at Swiss bank UBS and a former Fed official. “Throw Trump into the mix, and you’re in a completely different circumstance where he does like to drive the narrative.

“You just end up being dragged around,” he said.

The Fed has repeatedly pointed to trade tensions, slowing global growth and muted inflation as its main reasons for lowering rates, a move intended to support the economy as recession fears have begun to creep into the Treasury bond market.

But the economy is still growing, with consumer spending powering it forward and the labor market continuing to add jobs, suggesting some room for optimism about the future of the expansion, the longest in U.S. history.

The Fed has remained reticent to share details about its plans as it closely monitors the complicated economic picture. After the central bank lowered rates in July — its first cut in more than a decade — Powell suggested that the Fed wasn’t yet embarking on a full-blown cutting cycle. But markets are expecting several more reductions between now and early next year and will be watching the chairman closely for signals on that front.

But those decisions will be driven, at least in part, by the outcome of the U.S.-China trade war, meaning the Fed, like the rest of Washington, will continue to keep an eye on Trump’s Twitter storms.

Against that backdrop, Trump tweets, often daily, that the Fed is clueless and that if it would only slash rates by a large amount, the economy would take off like a “rocket ship.”

“The United States, because of the Federal Reserve, is paying a MUCH higher Interest Rate than other competing countries,” the president tweeted on Monday. “They can’t believe how lucky they are that Jay Powell & the Fed don’t have a clue,” he added, calling for a “Big Interest Rate Drop.”

His recent attempt to push the Fed to pursue negative interest rates — a move tried in Europe and Japan with unclear results — demonstrates the shift in who is controlling the narrative around the Fed.

A decade ago, the central bank pursued a range of new and untested policies to jump-start the economy — such as purchasing trillions of dollars in government bonds — and faced challenges in getting the public on board. Now, while the pursuit of negative rates in the U.S. would still be highly controversial, Trump is the one driving the conversation toward unconventional policies.

“There’s no escaping the president’s bully pulpit, no matter what it is he’s talking about, not the least when it comes in the form of a tweet where it gets promoted and dissected,” said Sarah Binder, a political science professor at George Washington University. “It focuses media attention. It focuses public attention.”

Trump has also urged the Fed to help him more directly fight his trade wars, focusing much of his frustration on the heft of the dollar, whose strength makes U.S. exports more expensive.

He has gone from suggesting the central bank cut its main borrowing rate by a whole percentage point — the equivalent of four standard cuts — to now calling for rates of “ZERO, or less,” which would mean lowering rates by at least 2 percentage points.

“He certainly is the big elephant in the room,” Binder said.

“If part of [Fed] communications is telling markets and the public and businesses where you’re headed, and if people wonder where they’re headed because the president has now injected himself into the debate … then that kind of undermines the whole use of communications as the central tool” of monetary policy, she added.

As for the Fed’s ultimate decisions on rates, Carpenter said he believes central bank officials when they insist that they do not discuss the political implications of their decisions at their policy meetings. But, he said, the pressure likely makes them more cautious.

“Their lives are just made that much more complicated by having to second-guess themselves, and saying, ‘OK, now we’ve made a decision, let’s ask ourselves one more time, are we sure we’re doing this for the right reasons?‘”

(Bloomberg) -- It had been more than a decade since Federal Reserve traders jumped into U.S. money markets to inject cash. And they seemed to get the reaction they wanted Tuesday morning, instantaneously driving down key short-term rates that had spiked to as high as 10% and threatened to muck up everything from Treasury bond trading to lending to companies and consumers.But the move didn’t last long.By the end of the trading session, rates were grinding back up, prompting Fed officials to fire off a second missive late in the day: They would be back Wednesday morning to offer another $75 billion of cash to the market. Overnight repurchase rates were being quoted at around 4% for Wednesday morning, according to Jefferies.

The moves underscored just how deep the structural problems in U.S. money markets have become. Namely, there is often not enough cash on hand at major Wall Street firms to meet the funding demands of a market trying to absorb record Treasury bond sales needed to fund U.S. budget deficits. The solution, according to longtime observers, would be for the Fed to continue to inject cash on a regular basis.

“The underlying problem is that there isn’t enough liquidity in the system to satisfy the demand and the job of the central bank is to provide such liquidity,” said Roberto Perli, a former Fed economist and partner at Cornerstone Macro in Washington. “What the Fed did was just a patch.”

A couple of catalysts caused the squeeze in repo liquidity. There was a big swath of new Treasury debt that settled into the marketplace -- adding to dealer balance sheet holdings -- just as cash was sucked out by quarterly tax payments companies needed to send to the government. If left unchecked, the escalation in rates could do damage to the broader economy by hiking borrowing costs for companies and consumers.

The timing couldn’t have been worse, with Fed leaders and many key New York Fed staffers gathered in Washington for a two-day policy meeting that will end Wednesday. Fed officials are widely expected to cut their target rate by a quarter-point. But the money-market problem threatens to overshadow that, as Wall Street is ready to find out what, if anything, the Fed might do to fix the situation for good.

“The increase in repo and other short-term rates is indicative of the reduced amount of balance sheet that financial intermediaries -- particularly primary dealers -- are either willing or able to provide those in search of short-term financing,” said Tony Crescenzi, market strategist at Pacific Investment Management Co. and author of a 2007 edition of “Stigum’s Money Market,” a widely read textbook first published in 1978. “It serves as a reminder of the challenges that investors could face in other ways if and when they seek to transfer risk -- sell their risk assets -- during a risk-off mode.”

This is far from the first bout of volatility in the over $2 trillion repo market, but eye-catching moves tend to happen only at quarter- or year-end when liquidity sometimes dries up -- not in the middle of the month, as it is now. Even setting aside this week’s huge spike, turmoil has been more pronounced following the 2008 crisis because reforms designed to safeguard the financial system have driven some banks out of this market. Fewer traders can lead to rapid swings by creating imbalances between supply and demand.

Fed interventions in the repo market, like the one deployed Tuesday and planned for Wednesday, were commonplace for decades before the crisis. Then they stopped when the central bank changed how it enacted policy by expanding its balance sheet and using a target rate band.

The tumult seen Monday and Tuesday doesn’t mean another global funding crisis, even though trouble getting funds through repo a decade ago doomed Lehman Brothers and almost snuffed out the global financial system.

But, many experts say, these wild few days show that there’s not enough reserves -- or excess money that banks park at the Fed -- in the banking system. That means traders are this week having to pay up to get these funds, even as bank reserves total more than $1 trillion. That means the Fed may again have to grow its $3.8 trillion balance sheet through quantitative easing, or debt purchases that create fresh reserves.

There are other remedies. The Fed has considered introducing a new tool, an overnight repo facility, that could be used to reduce pressure in money markets. And some strategists predict it may make another technical tweak to something called the interest rate on excess reserves on Wednesday, an attempt bring markets back in line.

“There were a confluence of factors that triggered the issues this week,” said Darrell Duffie, a Stanford University finance professor who’s co-authored research on repos with Fed staffers. “But the fact that it’s happening means something at the Fed should be done. For the Fed to be really confident in ending the issues, they will have to grow the balance sheet.”

The U.S. government has made matters worse over the past year by adding a record amount of new debt, and that will likely only increase as the deficit swells past $1 trillion. That has buoyed the amount of debt that dealers have on their balance sheets, and the repo market is one way they finance those positions. That said, their Treasury holdings are down from a peak in May, so that’s not necessarily behind this week’s big moves.

“Supply is a backdrop contributor to the issues, as there is just that much more collateral that needs to be financed,” said Seth Carpenter, a former adviser to the Fed Board of Governors who is now chief U.S. economist at UBS Securities LLC. “The market is still trying to deal with tight balance sheets from dealers. Overall this is all part the market shifting through time to a new set of realities.”

(Adds Wednesday’s repo rate quote in third paragraph)

(Reuters) - As if the U.S. Federal Reserve didn’t already have enough on its plate heading into its meeting on interest rates this week, chaos deep inside the plumbing of the U.S. financial system has thrown policymakers an unexpected curveball.

FILE PHOTO: Federal Reserve Board building on Constitution Avenue is pictured in Washington, U.S., March 19, 2019. REUTERS/Leah Millis/File Photo

Cash available to banks for their short-term funding needs all but dried up on Monday and Tuesday, and interest rates in U.S. money markets shot up to as high as 10% for some overnight loans, more than four times the Fed’s rate.

That forced the Fed to make an emergency injection of more than $50 billion, its first since the financial crisis more than a decade ago, to prevent borrowing costs from spiraling even higher. It will conduct another one on Wednesday.

The exact cause of the squeeze is a matter of some debate, but most market participants agree that two coincidental events on Monday were at least partly to blame. First, corporations had to withdraw funds from money market accounts to pay for quarterly tax bills, and then on the same day the banks and investors who bought the $78 billion of U.S. Treasury notes and bonds sold by Uncle Sam last week had to settle up.

On top of that, the reserves that banks park with the Fed and are often made available to other banks on an overnight basis are at their lowest since 2011 thanks to the central bank’s culling of its vast portfolio of bonds over the past few years.

Added together, these factors are testing the limits of the $2.2 trillion repurchase agreement - or repo - market, a gray but essential component of the U.S. financial system.

Whatever the cause, the episode has added fuel to the argument that the Fed needs to take steps to avoid more disruptions in the repo market down the road.

The repo market underpins much of the U.S. financial system, helping to ensure banks have the liquidity to meet their daily operational needs and maintain sufficient reserves.

In a repo trade, Wall Street firms and banks offer U.S. Treasuries and other high-quality securities as collateral to raise cash, often overnight, to finance their trading and lending activities. The next day, borrowers repay their loans plus what is typically a nominal rate of interest and get their bonds back. In other words, they repurchase, or repo, the bonds.

The system typically hums along with the interest rate charged on repo deals hovering close to the Fed’s benchmark overnight rate, currently set in a range of 2.00% to 2.25%. That rate is expected to be cut by a quarter percentage point on Wednesday.

But sometimes, investors get fearful of lending, as seen during the global credit crisis, or at other times there are just not enough reserves or cash in the system to lend out, as appeared to be the case this week. And that can cause a squeeze on the market and send borrowing costs zooming higher.

But when investors get fearful of lending, as seen during the global credit crisis, or when there are just not enough reserves or cash in the system to lend out, it sends the repo rate soaring above the Fed Funds rate.

Trading in stocks and bonds can become difficult. It can also pinch lending to businesses and consumers and, if the disruption is prolonged, it can become a drag on a U.S. economy that relies heavily on the flow of credit.

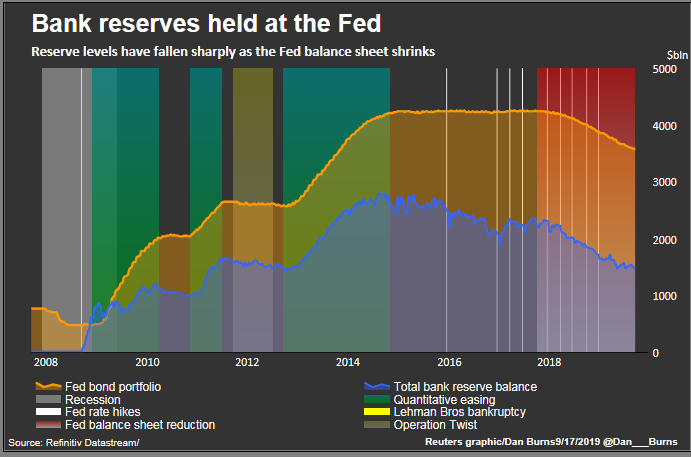

WHAT HAS CAUSED THE DROP IN BANK RESERVES?

Coming out of the financial crisis, after the Fed cut interest rates to near zero and bought more than $3.5 trillion of bonds, banks built up massive reserves held at the Fed.

But that level of bank reserves, which peaked at nearly $2.8 trillion, began falling when the Fed started raising interest rates in late 2015. They fell even faster when the Fed started to cut the size of its bond portfolio about two years later.

The Fed stopped raising interest rates last year and cut them in July and is expected to do so again on Wednesday. It has also now ceased allowing to bonds to roll off its balance sheet.

The question vexing policymakers now is whether those actions are enough to stop the downward drift in reserves, which are a main source of liquidity in funding markets like repo.

Bank reserves at the Fed last stood at $1.47 trillion, the lowest level since 2011 and nearly 50% below their peak from five years ago.

Through the Federal Reserve Bank of New York, the Fed can conduct occasional spot repo operations at times of funding stress, allowing banks and dealers to swap their Treasuries and other high-quality securities for cash at a minimal interest rate. It did this on Tuesday and will do it again on Wednesday.

2. LOWER THE INTEREST IT PAYS ON EXCESS RESERVES

By making it less profitable for banks, especially foreign ones, to leave their reserves at the Fed, it may encourage banks to lend to each other in money markets.

3. CREATE A STANDING REPO FACILITY

Such a permanent financing program will allow eligible participants to exchange their bonds for cash at a set interest rate.

Fed and its staff have considered such a facility, but they have not determined who qualifies, what would be the level of interest paid and the timing for a possible launch.

4. RAMP UP BUYING OF TREASURIES

The Fed can replenish the level of bank reserves by slightly increasing its holdings of U.S. government debt. This comes with the risk that it may be perceived as a resurrection of quantitative easing rather than a technical adjustment.

Reporting by Richard Leong; Editing by Dan Burns and Richard Borsuk

Boeing Dreamliner 787 Air China planes sit on the production line at the company's final assembly facility in North Charleston, South Carolina.

Travis Dove | Bloomberg | Getty Images

Boeing has claimed that growing Chinese demand for planes will generate almost $3 trillion worth of industry business over the next two decades.

In its latest market outlook, the U.S. plane maker predicts China will soon become the world's largest aviation market and will need 8,090 new planes by 2038. Boeing believes within a decade that one-in-five airline passengers will be Chinese.

The figure would equate to $1.3 trillion in current list prices. Boeing said associated services to maintain fleets would be even larger at $1.6 trillion, meaning almost $3 trillion worth of business could be up for grabs.

Boeing has said passenger traffic within China is tipped to grow at more than 6% a year until 2038 and China's middle class is expected to double in size within a decade.

While domestic flights are predicted to provide the lion's share of growth, outward bound international travel will also increase.

"An expanding middle class, significant investment in infrastructure, and advanced technologies that make airplanes more capable and efficient, continue to drive tremendous demand for air travel," said Randy Tinseth, vice president of commercial marketing for Boeing said in a statement Tuesday.

China's need for new and replacement planes between now and 2038 are broken down by Boeing's analysts into 5,960 single-aisle jets, 1,780 widebody planes, 230 freighters, and 120 regional jets.

On a global basis, Boeing is projecting $6.8 trillion worth of airplane sales by 2038 with a further $9.1 trillion in services.

More than 2000 Boeing planes have already been delivered to China with around a quarter of the plane makers production line now delivered to Chinese customers. Boeing has said one third of its 737 planes are currently delivered to China.

The 737 Completion & Delivery Center in Zhoushan is a joint venture between Boeing and Commercial Aircraft Corporation of China, Ltd (COMAC). It was built to provide interior furnishings and exterior paint to planes that have arrived from Seattle.

In December last year, Air China received a 737 Max 8 which was the first Boeing plane to be completed in China for a local customer.

But on March 11, China ordered its airlines to suspend operations of their 737 MAX 8 planes following two fatal crashes of the model within 5 months. In a sign of China's growing importance as an aviation regulator, most other agencies and airlines followed suit over the next two days.

{kind=link}

{kind=link}