President Donald Trump has called Federal Reserve Chairman Jerome Powell 'clueless.' | Drew Angerer/Getty Images

President Donald Trump has taken over Jerome Powell’s life.

The Federal Reserve’s expected decision on Wednesday to cut interest rates again will spark new questions about whether Powell, its chairman, is caving to intense public pressure by Trump. While Powell strongly rejects that notion, the president’s policies have clearly forced the central bank’s hand.

Story Continued Below

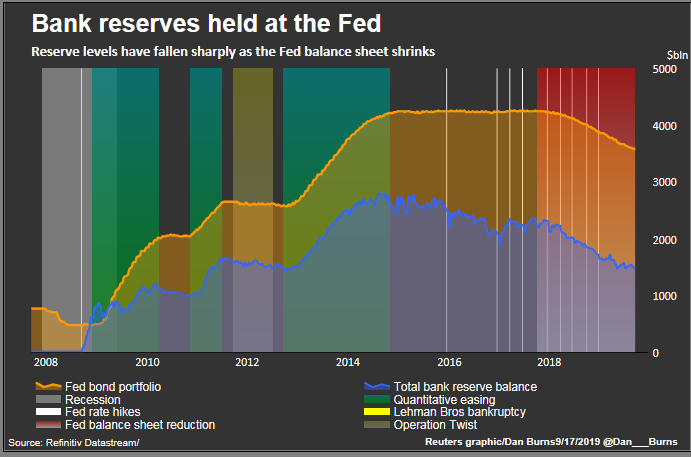

The Fed, which last December was considering hiking interest rates at least twice this year, has done a head-spinning turn since then in response to weakening business investment, a contraction in manufacturing and a global slowdown — all fueled by Trump’s trade wars.

And the president’s abrupt decision last year to pull out of the Iran nuclear accord arguably set off a steady deterioration in relations that today has made Middle East tensions another threat to economic growth that the Fed must take into account.

Trump is forcing still more dramatic policy options into the limelight — including his latest call on the Fed to cut rates below zero, an idea that the central bank has long resisted as an avenue for fighting recessions.

“I’ve always thought the Fed has been a little bit slow to control the narrative about monetary policy,” said Seth Carpenter, chief U.S. economist at Swiss bank UBS and a former Fed official. “Throw Trump into the mix, and you’re in a completely different circumstance where he does like to drive the narrative.

“You just end up being dragged around,” he said.

The Fed has repeatedly pointed to trade tensions, slowing global growth and muted inflation as its main reasons for lowering rates, a move intended to support the economy as recession fears have begun to creep into the Treasury bond market.

But the economy is still growing, with consumer spending powering it forward and the labor market continuing to add jobs, suggesting some room for optimism about the future of the expansion, the longest in U.S. history.

The Fed has remained reticent to share details about its plans as it closely monitors the complicated economic picture. After the central bank lowered rates in July — its first cut in more than a decade — Powell suggested that the Fed wasn’t yet embarking on a full-blown cutting cycle. But markets are expecting several more reductions between now and early next year and will be watching the chairman closely for signals on that front.

But those decisions will be driven, at least in part, by the outcome of the U.S.-China trade war, meaning the Fed, like the rest of Washington, will continue to keep an eye on Trump’s Twitter storms.

Against that backdrop, Trump tweets, often daily, that the Fed is clueless and that if it would only slash rates by a large amount, the economy would take off like a “rocket ship.”

“The United States, because of the Federal Reserve, is paying a MUCH higher Interest Rate than other competing countries,” the president tweeted on Monday. “They can’t believe how lucky they are that Jay Powell & the Fed don’t have a clue,” he added, calling for a “Big Interest Rate Drop.”

His recent attempt to push the Fed to pursue negative interest rates — a move tried in Europe and Japan with unclear results — demonstrates the shift in who is controlling the narrative around the Fed.

A decade ago, the central bank pursued a range of new and untested policies to jump-start the economy — such as purchasing trillions of dollars in government bonds — and faced challenges in getting the public on board. Now, while the pursuit of negative rates in the U.S. would still be highly controversial, Trump is the one driving the conversation toward unconventional policies.

“There’s no escaping the president’s bully pulpit, no matter what it is he’s talking about, not the least when it comes in the form of a tweet where it gets promoted and dissected,” said Sarah Binder, a political science professor at George Washington University. “It focuses media attention. It focuses public attention.”

Trump has also urged the Fed to help him more directly fight his trade wars, focusing much of his frustration on the heft of the dollar, whose strength makes U.S. exports more expensive.

He has gone from suggesting the central bank cut its main borrowing rate by a whole percentage point — the equivalent of four standard cuts — to now calling for rates of “ZERO, or less,” which would mean lowering rates by at least 2 percentage points.

“He certainly is the big elephant in the room,” Binder said.

“If part of [Fed] communications is telling markets and the public and businesses where you’re headed, and if people wonder where they’re headed because the president has now injected himself into the debate … then that kind of undermines the whole use of communications as the central tool” of monetary policy, she added.

As for the Fed’s ultimate decisions on rates, Carpenter said he believes central bank officials when they insist that they do not discuss the political implications of their decisions at their policy meetings. But, he said, the pressure likely makes them more cautious.

“Their lives are just made that much more complicated by having to second-guess themselves, and saying, ‘OK, now we’ve made a decision, let’s ask ourselves one more time, are we sure we’re doing this for the right reasons?‘”

https://www.politico.com/story/2019/09/18/trump-federal-reserve-jerome-powell-interest-rates-1500930

2019-09-18 09:02:00Z

52780383489542

{kind=link}

{kind=link}